M&A is gaining attention as a strategy for startups to expand their businesses. In this panel moderated by MUFG Innovation Partners (MUIP) Chief Investment Officer Takashi “Taka” Sano, newmo’s CEO Naoki Aoyagi, who executed two acquisitions within just a year of the company’s founding in January 2024, Kanmu’s CEO Wataru Yamaki of Kanmu, which became a member of Mitsubishi UFJ Financial Group (MUFG),

and Yoshihide Hiroto of AGS Consulting, a firm with extensive experience in supporting IPOs, discuss their experience.

Startups’ evolving growth strategies

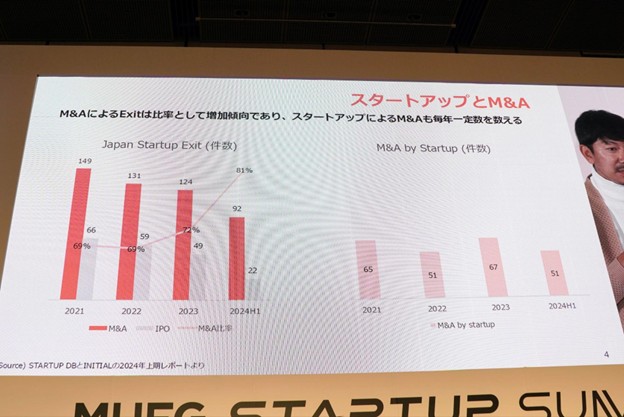

In Japan, IPOs have traditionally been the primary exit strategy for startups. The IPO market has experienced significant fluctuations, reaching around 200 listings per year in the 1990s and is recently just under 100 listings annually.

M&A is fast becoming a prominent exit option for startups amidst this market shift. According to Yoshihide Hiroto, CEO of AGS Consulting, which has supported over 200 IPOs, there has been a noticeable rise in M&A deals involving startups in recent years.

Hirowatari explained the two key characteristics of this shift. The first is the proactive use of M&A before IPOs. Traditionally, startups tended to avoid acquisitions before going public due to concerns about regulatory scrutiny. However, a new strategy is emerging - one where companies actively leverage M&A to bring in key partners before listing, all in pursuit of their broader vision.

Taka illustrated this shift with a graph, highlighting a reversal in IPO and M&A trends. Since 2021, a year of significant changes in public markets, IPOs have been on the decline, while M&A activity has increased.

A major factor behind this trend is the evolving fundraising environment for startups. “Compared to seven or eight years ago, the amount of capital raised has tripled or even quintupled. The number of VCs has grown, and as each fund delivers strong performance, fund sizes have expanded,” noted newmo’s Aoyagi.

The second key trend is the rise of the dual-track strategy, where startups pursue both IPOs and the possibility of joining a larger group through M&A.

Recent success stories of this approach include Soracom, which went public in March 2024 after being under KDDI, and dely, which listed in December 2024 after operating under LINE Yahoo. Hirowatari emphasized that these “swing-by IPOs“ demonstrate the growing importance of the dual-track strategy in today’s startup landscape.

Executing M&As in pursuit of growth

newmo has been actively leveraging M&A for growth. Founded in January 2024, the company executed two acquisitions within just one year. It also secured significant funding, raising approximately JPY 2 billion in its seed round and an impressive JPY 16.7 billion subsequently in its Series A round.

newmo’s strategy is clear: build on its taxi business as a foundation while integrating ridesharing and fintech to create a new regional mobility ecosystem. “We are improving the management of taxi operators while using that foundation to expand into ridesharing,” explains Aoyagi.

In Osaka, for example, newmo operates 11 branches and is upgrading its taxi business by integrating its proprietary ride-hailing app. What is notable is how the company managed to advance both fundraising and M&A in parallel.

The choice of joining a major corporate group through M&A

On the other hand, Kanmu, which operates a mobile prepaid card business, joined a major corporate group through M&A. In March 2023, the company became a consolidated subsidiary of Mitsubishi UFJ Financial Group (MUFG).

Kanmu’s main service is the VISA prepaid card “Vandle Card.” As of December 31, 2022, when it announced a capital and business alliance with MUFG, the card had surpassed 6 million downloads (Note: by February 28, 2024, it had exceeded 10 million). The company was also expanding into new business areas, including the “Pool” credit card, which offers up to 2% annual interest when funds are deposited

The selection of a partner took nearly a year, during which Kanmu held discussions with multiple candidates. “In discussing the business, we kept it light at first, focusing on making sure both sides were clear about their goals,” Yamaki reflects. While the valuation of the company was an important factor, “we also focused on ensuring there was synergy and that the partner could provide the stability needed for operating capital to help grow the business.”

The nature of the prepaid card business as a financial sector venture also influenced this decision. “If we had remained independent, I think fundraising would have been a constant struggle,” Yamaki admitted candidly. As the business scaled, the need for operating capital was expected to grow significantly.

Post-merger integration is key to M&A success

The true value of M&A is tested during the post-merger integration (PMI) process. In this regard, the approaches of newmo and Kanmu have been quite different.

In the case of newmo, the company quickly implemented a clear 100-day integration plan immediately after the acquisition. The M&A team expanded rapidly from an initial three members to about 10 now, running approximately 20 projects concurrently.

A particularly important aspect of this integration was the introduction of management accounting at the operational level of the taxi company’s branches. “We didn’t even know which branches were profitable or losing money,” Aoyagi explains. By clarifying the operational efficiency of each branch and setting clear goals, the company made significant progress.

Aoyagi also emphasized what he calls “emotional PMI” involving building human relationships. “The real situation, which we couldn’t see until the contracts were signed, only becomes clear afterward. With that, we built relationships to gradually tackle the harder challenges.” He splits his time between Osaka and Tokyo, frequently visiting branches to foster trust with the on-the-ground staff.

On the other hand, Kanmu, due to its integration into a large financial group, took a more cautious approach. Yamaki recalls, “At first, I didn’t understand who was saying what in such a big company. It took me a while to figure out how things worked beyond just the organizational chart. Recently, I’ve started to understand which buttons to push to get things moving.”

Yamaki highlighted the importance of communication with the frontline staff during integration. Since they had shared information with a considerable number of people from the early stages of the capital and business alliance discussions, the company was able to execute the integration announcement with minimal resistance.

Startup M&As are no longer rare

The use of M&A by startups is likely to grow. Hirowatari points out that M&A, including its methods, are beginning to be understood. It’s no longer just a simple matter of big companies making acquisitions because they have money. Instead, more strategic and diverse approaches are becoming possible. To succeed, however, a clear strategic intent is essential.

He warns, “If you say, ‘We acquired a startup because we were interested,’ that’s not enough. M&A becomes a business only when it is driven by a strategy.”

For startups considering future M&As, especially those considering joining a corporate group, Yamaki offers specific advice: “It’s better to ask institutional investors, ‘What do you think would happen if we did this with this company?’”

This is especially important when pursuing a swing-by IPO, a term referring to a parent-child listing. While investors may expect a certain impact on the profit and loss statement, if the impact is around 40-50%, it could raise concerns about the startup’s independence. Striking the right balance amongst these factors is crucial.

Aoyagi expressed a cautious yet optimistic view on the market environment: “Since around 2021, the market has indeed been in a winter phase, but thanks to initiatives like the ‘Startup Development Five-Year Plan,’ it hasn’t deteriorated as much as expected. While it’s unclear whether there will be a rapid recovery next year, in the broader picture, both the IPO and M&A markets will improve.”

Aoyagi expressed his hope for the startup ecosystem, saying, “I hope we can carry forward the knowledge we’ve gained, much like how we learned from GENDA (a publicly listed startup that widely expanded its entertainment business and used M&A strategically). It would be great if more startups took on similar challenges.”

The experiences of the panelists show that the use of M&A by startups is no longer a rare occurrence and is increasingly being recognized as a crucial growth strategy option.

![]()